In our current financial marketplace, maintaining deep liquid reserves represents a vital core requirement before attempting to deploy capital into volatile growth vehicles. Whether you are initiating a basic individual budgeting structure or managing cash-flow distributions across a complex entrepreneurial launch, understanding structural sizing matrices gives you an unmatched competitive edge, insulating your active positions from forced liquidations during sudden economic downturns.

This master guide unpacks the mechanics of liquid safety architectures, evaluates structural sizing benchmarks, maps automated positioning engines, reviews business safety blueprints, details real financial validation structures, and outlines the precise review roadmap to achieve true operational resilience in 2026.

This master guide unpacks the mechanics of liquid safety architectures, evaluates structural sizing benchmarks, maps automated positioning engines, reviews business safety blueprints, details real financial validation structures, and outlines the precise review roadmap to achieve true operational resilience in 2026.

Defining Emergency Savings Liquidity Parameters

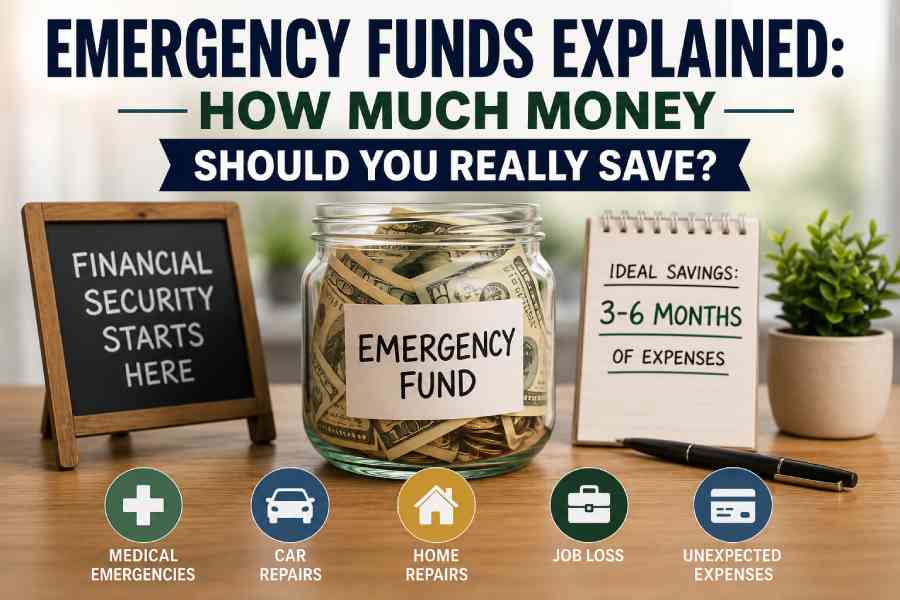

An emergency fund is a separate, highly protected capital pool allocated specifically to absorb unforeseen lifestyle expenses or sudden cash-flow drops. Unlike standard equity tranches or real estate investments built for compounding growth, emergency accounts prioritize capital preservation, low volatility, and instant accessibility over total performance yield.

The primary baseline operational focus requires maintaining an immediate buffer that stays decoupled from broader market drawdowns. This safety layer is strictly reserved to address un-projected liabilities—such as urgent health adjustments, corporate employment pauses, structural transport replacements, or insurance deductibles—ensuring discretionary choices never tap into protective holdings.

Strategic Benefits of Structural Cash Safeguards

Maintaining solid, non-volatile cash buffers gives you immense flexibility across all sectors of your financial plan. When unexpected liabilities occur, individuals lacking capital protection often resort to high-interest credit lines or early retirement account withdrawals, both of which quietly destroy long-term compounding velocity.

By establishing an organic cash layer, you eliminate high-interest vulnerabilities, lower structural anxiety, and gain the time needed to evaluate market adjustments calmly. This positioning serves as a fundamental capital protection prerequisite before you expose a single dollar to the volatility of open market trading screens.

Determining Your True Target Reserve Size

There is no single baseline capital target that perfectly balances every single domestic structure or operational business unit. Modern cash management planning requires creating custom allocation sizes based on employment stability and income predictability.

| Professional Workflow Category | Target Liquidity Runway | Operational Baseline Focus |

|---|---|---|

| Stable Institutional Corporate Employee | 3–4 Months of Fixed Cost Outflow | Low overhead risk insulation |

| Variable Bonus/Commission Earner | 6–9 Months of Fixed Cost Outflow | Smoothing transaction pipeline gaps |

| Independent Freelancer / Agency Owner | 9–12 Months of Fixed Cost Outflow | Insulating against volatile client contract adjustments |

| Single-Income Family Unit | 6–12 Months of Fixed Cost Outflow | High dependent overhead security |

| Retired Portfolio Wealth Consumer | 12+ Months of Fixed Cost Outflow | Total mitigation of sequence-of-returns risk |

Core Lifestyle Variables and Income Dynamics

Calibrating your final target size requires evaluating several key lifestyle variables:

- Income Visibility: High-variance freelancers or business partners require significantly larger protective cash cushions than salaried public sector employees.

- Dependent Overhead: Households with multiple dependents, active healthcare liabilities, or older infrastructure must carry deep liquidity tranches.

- Debt Structure: High fixed obligations—such as residential commercial mortgages or corporate operational lines—demand a wider safety margin.

Allocation Selection: Secure Liquid Storage Vehicles

Where you park your emergency capital is just as critical as the size of the fund itself. Because your primary goals are capital preservation and instant availability, you must prioritize low-risk options over high performance yields.

The Operational Reality of Investing Cash Reserves: Placing your emergency tranches into volatile common stocks, speculative sector funds, or digital crypto assets exposes your safety layer to sudden market downturns. If a crisis hits during a market drop, you could be forced to liquidate your holdings at a significant loss, locking in damages permanently.

To avoid this, store your safety reserves inside highly secure, liquid environments—such as certified high-yield savings accounts (HYSAs) or conservative money market products that deliver competitive yields while providing next-day withdrawal access.

Business Safety Engineering: Budget Templates & Pitching

As market demand for automated savings tools grows, financial technology firms are scaling specialized cash-management applications, automated micro-saving scripts, and unified banking dashboards. Launching a platform in this space requires a highly structured business framework to navigate compliance audits and secure growth funding successfully.

The Financial Platform Business Plan Template Structure

Before launching an automated savings app, your internal corporate business plan template must follow this structured, five-part framework:

- Executive Value Proposition: Define the exact user friction your software addresses—such as using smart algorithms to automatically route a user’s excess cash into high-yield accounts based on their custom spending habits.

- Regulatory & Compliance Layer: Map your partnerships with cleared banking networks, custodial security structures, and automated compliance protocols to ensure full legal alignment.

- Technology Architecture & Security: Document your real-time data sync maps, data encryption standards, and platform connection pipelines to protect consumer cash records perfectly.

- User Acquisition Funnel: Detail your strategy for driving organic traffic through comprehensive financial literacy content, minimizing user acquisition costs (CAC) over time.

- Platform Monetization Model: Outline your revenue streams—including transparent SaaS software subscriptions, minor transaction commissions, or tiered corporate pricing levels.

Structuring a Venture Capital Investor Pitch

Venture capital groups and financial technology syndicates look past general market enthusiasm to analyze your software’s user retention loops and data security frameworks. When pitching an automated cash management application, your deck must clearly deliver three core metrics within the initial review slides:

- User Engagement & Retention Trajectories: Present clear data proving that your platform’s budgeting tools keep users active over long horizons, increasing customer lifetime value (LTV).

- Data Pipeline Security Validation: Demonstrate that your software architecture has passed complete external penetration tests, eliminating data leak vulnerabilities.

- Regulatory Asset Protection: Prove that your financial clearings routes use fully insured account pipelines, giving users complete safety peace of mind.

Corporate Projection Models: Cash Safety Sizing

A smart fintech platform’s financial projections should always avoid arbitrary growth estimates. Instead, they must be built directly from core operational metrics, such as cloud hosting requirements, banking API connection licensing fees, and proven customer acquisition trends.

The table below breaks down a realistic three-year financial scaling model for an automated personal savings platform transitioning into high-efficiency enterprise scaling:

| Platform Performance Metric | Year 1 (Alpha Launch) | Year 2 (Market Scaling) | Year 3 (Enterprise Dominance) |

|---|---|---|---|

| Gross Software Subscription Revenue | $210,000 | $980,000 | $3,400,000 |

| Data Pipeline & Core Cloud Infrastructure | $38,000 | $110,000 | $260,000 |

| Regulatory Compliance & Legal Oversight | $55,000 | $130,000 | $290,000 |

| Organic Content & Search Marketing | $32,000 | $160,000 | $420,000 |

| Net Operating Profit Margin Percentage | 40.4% | 59.1% | 71.4% |

| Realized Net Annual Profits | $85,000 | $580,000 | $2,430,000 |

When presenting these data grids during institutional funding rounds, you must always explicitly state your baseline assumptions—including targeted platform price levels, average user account lifetimes, and organic client acquisition speeds.

Real-World Case Studies: Defensive Capital Management

To see how disciplined liquidity allocation and automated safety platforms perform in real-world environments, let’s analyze two realistic case studies.

Case Study 1: Rebalancing Individual Safety via Algorithmic Cash Positioning

A senior network architecture engineer earning a high annual salary struggled with lifestyle inflation. Despite their steady income, they carried less than $5,000 in liquid savings because they over-allocated capital into highly volatile tech sector stocks. When their company announced a surprise corporate restructure that paused their contract for 90 days, they faced immediate financial stress and were nearly forced to sell their stock positions at a 22% market loss.

Their strategy shifted when they adopted Habit 1 (Expense Tracking) and built a dedicated 6-month safety buffer using a structured Business Plan Template. They automated 25% of their monthly cash flow directly into high-yield savings pipelines. When their contract experienced a second unexpected adjustment a year later, their cash buffer covered all fixed obligations smoothly, protecting their core equity portfolios from forced liquidations.

Case Study 2: Scaling an Automated Micro-Savings App

Let’s look at a digital finance startup that wanted to offer automated savings tracking to younger retail users but faced high onboarding friction and strict data-compliance audits. By building their application using a validated business template, they automated core processes like risk scoring, programmatic cash sweeping, and multi-account balance optimization.

The platform used their initial transaction volume data to secure a $500,000 institutional seed investment. By utilizing low-overhead automated indexing tools to manage user accounts efficiently, the app scaled its active user base from 4,500 accounts to over 95,000 accounts within 24 months, proving that smart capital safety software can build a highly profitable enterprise while driving massive user adoption.

Critical Allocation Mistakes to Avoid Completely

Building a resilient financial safety layer requires maintaining lean cost structures and avoiding emotional execution traps. Watch out for these common cash management mistakes:

- Using Emergency Reserves for Discretionary Spending: Allowing your liquid safety cash to fund impulse luxury items, vacations, or lifestyle enhancements, breaking your safety structures.

- Over-Allocating Capital to Volatile Vehicles: Keeping your primary safety reserves inside high-risk assets that are exposed to unexpected market corrections.

- Failing to Adjust for Inflation Changes: Neglecting to audit your fixed monthly expenses annually, leaving your safety buffer too small to match rising real-world living costs.

- Operating Without Automated Deposit Funnels: Relying on manual human willpower to build your savings instead of using programmatic payroll transfers to fund your reserves instantly.

Actionable Financial Preparedness Checklist

Use this comprehensive operational checklist once a quarter to ensure your capital safety buffers remain secure, efficient, and fully optimized:

- Audit all bank statements from the past 90 days and calculate your exact fixed monthly living costs.

- Verify that your automated transfer pipelines are routing capital correctly on your platform on payday.

- Ensure your cash safety buffer holds at least 3 to 6 months of necessary living costs, adjusted for inflation.

- Audit the current interest yields and fee structures on your savings accounts to maximize efficiency.

- Confirm that your emergency cash remains decoupled from your active stock trading and investment portfolios.

- Dedicate 2 hours to researching updated data security guidelines and regional compliance standards.

Conclusion & Next Tactical Steps

An optimized emergency fund is far more than a simple savings account—it is a vital, strategic framework designed to help you navigate economic uncertainty with complete confidence. Whether you face unexpected contract adjustments, sudden healthcare liabilities, or broader market corrections, carrying deep cash reserves ensures your financial foundation remains stable, protecting your active long-term investments from forced liquidations.

Long-term financial success relies on moving past speculative debates and focusing instead on systematic capital engineering. By setting realistic protection milestones, automating your savings contributions, and utilizing comprehensive planning templates, you can successfully manage changing market cycles.

Don’t wait for a major economic shift to expose vulnerabilities in your plan. Audit your monthly fixed costs today, optimize your automated savings transfers, and build the resilient foundation your financial freedom deserves.

{kind=link}