At the same time, technological innovation provides access to powerful budgeting tools, investment platforms, banking applications, and financial education resources that previous generations never experienced.

At the same time, technological innovation provides access to powerful budgeting tools, investment platforms, banking applications, and financial education resources that previous generations never experienced.

Building sustainable financial habits early in life can significantly influence long-term wealth accumulation, financial security, and overall well-being.

This comprehensive guide explores practical smart budgeting tips for Millennials and Gen Z in 2026.

Why Budgeting Matters More Than Ever in 2026

Budgeting serves as the foundation of personal financial management. Without a clear understanding of income and expenses, individuals may struggle to save money, reduce debt, or achieve long-term financial goals.

Economic uncertainty continues to influence consumer behavior, making financial planning increasingly essential. Effective budgeting enables people to control spending, increase savings, reduce financial stress, and prepare for emergencies efficiently.

Millennials and Gen Z are uniquely positioned to leverage digital tools and financial technologies to simplify budgeting and improve money management.

Financial Challenges Facing Millennials and Gen Z

Younger generations face several financial obstacles that differ significantly from those experienced by earlier generations:

- High housing costs and rising macro inflation

- Student loan debt and increased healthcare expenses

- Gig economy income fluctuations and baseline retirement uncertainty

- Social media peer spending pressures and overall economic volatility

Recognizing these challenges allows individuals to design more realistic budgeting strategies.

Tip 1: Track Your Spending Habits

Many people underestimate how much they spend each month. Small purchases such as coffee subscriptions, online shopping, food delivery, and entertainment services can accumulate quickly. Tracking expenses provides visibility into financial behavior and identifies opportunities for improvement.

Methods for Tracking Spending:

- Mobile banking applications and account statement analysis

- Custom expense tracking spreadsheets or digital financial dashboards

- Consistent monthly spending reviews

Tip 2: Use Budgeting Applications

Technology has simplified budgeting significantly. Numerous applications now automate expense categorization, spending analysis, and savings tracking. Digital tools let users monitor real-time transactions, establish custom financial limits, and set spending benchmarks safely.

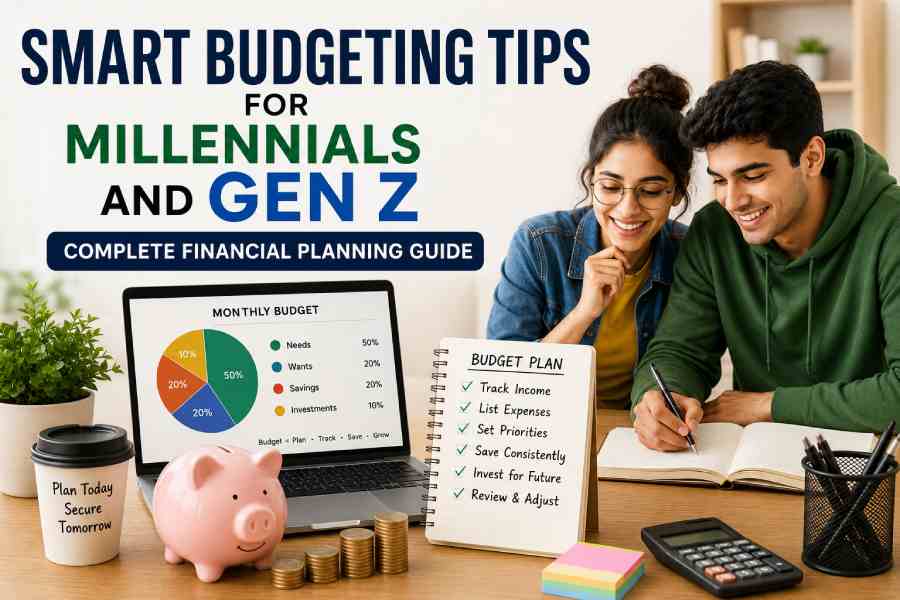

Tip 3: Follow the 50/30/20 Budgeting Rule

The 50/30/20 budgeting method remains one of the simplest and most effective approaches to personal finance:

- 50% for Essential Expenses: Rent, utilities, insurance, and groceries.

- 30% for Discretionary Spending: Dining out, entertainment, and hobbies.

- 20% for Savings and Investments: Retirement funds, emergency reserves, and market assets.

This framework creates a healthy balance between enjoying life today and preparing for future financial stability.

Tip 4: Build an Emergency Fund

Unexpected expenses can arise at any time. Medical emergencies, sudden job changes, urgent car repairs, and unexpected economic disruptions can instantly place immense pressure on your daily finances.

Financial experts commonly recommend saving between three and six months of core living expenses in a dedicated, liquid account to bypass reliance on high-interest debt instruments.

Tip 5: Avoid Lifestyle Inflation

As income increases, many individuals expand their lifestyle spending proportionally. This phenomenon is known as lifestyle inflation or lifestyle creep. Saving pay raises, automating structural investment contributions, and maintaining pre-raise spending benchmarks are critical paths to accelerating wealth creation.

Budgeting Framework Comparison

| Budgeting Method | Best For | Main Advantage | Difficulty Level |

|---|---|---|---|

| 50/30/20 Rule | Beginners | Simple allocation system | Easy |

| Zero-Based Budgeting | Detailed planners | Complete expense control | Moderate |

| Pay Yourself First | Savers and investors | Prioritizes wealth building | Easy |

| Values-Based Budgeting | Goal-oriented individuals | Aligns spending with priorities | Moderate |

| Cash Envelope Method | Overspenders | Improves spending discipline | Easy |

Financial Wellness Habits for Young Adults

Budgeting should be viewed as part of a larger, comprehensive financial wellness strategy. Sustainable habits contribute far more to long-term success than short-term austerity measures.

Habits That Support Financial Stability:

- Review cash outlays weekly and set strict measurable goals

- Scale up your personal annual savings percentages alongside income increments

- Automate investing channels and audit long-term credit profiles regularly

Future Budgeting Trends in 2026

Technology continues to deeply reshape personal finance management. Millennials and Gen Z are increasingly adopting digital-first, automated systems that drop calculation friction:

- AI-powered predictive budgeting and automated micro-savings sweeps

- Centralized subscription cancellation dashboards and intelligent cash flow forecasting algorithms

- Behavioral data notifications tracking real-time transaction speeds

How Budgeting Supports Financial Independence

Financial independence reflects having sufficient liquid assets, equity investments, and cash safety margins to support key lifestyle paths without depending entirely on traditional employment wages. Structural budgeting serves as the blueprint engine that feeds your investments consistently, keeping you insulated during unexpected career pivots or macro economic shifts.

Featured Snippet: Smart Budgeting Tips for Young Adults

The most practical budgeting tips for Millennials and Gen Z in 2026 include utilizing automated budgeting apps for expense categorization, tracking weekly transactions, implementing the 50/30/20 structure, capping lifestyle inflation when earnings rise, and securing a distinct 3-to-6-month liquid emergency fund.

Conclusion

Budgeting in 2026 has transitioned far beyond manual logging and retroactive spreadsheets. By capitalizing on smart automated technologies, anchoring clean saving habit loops, and tracking cash distributions via clear structural frameworks, young adults can comfortably insulate their financial future against changing macro economic trends.

{kind=link}